Apollo Global Management - The Next Berkshire

Why I am interested in Apollo:

My overall investment framework is centered on investing in key industries in China and US. For China it’s manufacturing and native technology platforms, so we have invested in BYD, Shemar Electric, and YMM. For US we believe its technology, financial services, Medtech/consumer. Currently we are underweight US because valuations, but once they reached a reasonable level we would like to buy technology companies (either indivisual or etf) and I have been actively searching for financial services companies that matches our investment preferences, I believe Apollo could be the best candidate for reasons I will explain below. We also have a venture portfolio that includes other ideas that we liked but couldn’t build a sizeable position on due to limited research capacity or high risk profile. Companies like Transmedics, Roadrunner, and KSPI fits under the venture bucket. These three constitutes our portfolio and will be dynamically rotated based on risk to reward profile and valuations.

So, back to Apollo, based on my conversation with professors and my own experience talking to college undergraduate students, I've observed that Stern’s top students used to aspire to go to elite investment banks like Goldman Sachs, but nowadays many are heading to straight to the buy‐side—companies like Apollo and Blackstone. Even the smartest talent on Wall Street is switching over to these firms. As Apollo’s CEO Marc Rowan said, asset management is essentially about selling judgment (financial advice on the sell side). Judgements are made by people, talented ones make great judgements that yield the firm alpha. This shift and aggregation of human talent in one firm made me curious and want to further investigate.

Furthermore, Stern has introduced a lot of courses on alternative assets in recent years—covering topics such as real estate and credit restructuring. The administrators at Stern are trying to diversify from investment banking and expose students to an array of career paths in high finance, and so far we have great placements into elite buyside firms. Going to these classes on alternative investments taught by wall street veterans really opened my eyes outside of equity market. I believe alternative assets like real estate and private credit will outperform vanilla portfolio of stock and bonds. And asset managers, in search of a higher yield, will allocate increasing part of their portfolio to alternative assets. This is a long term trend similar to when mutual fund was first created that helped retail investors to pool their assets and invest with professional manager, or when index funds was first introduced and how it has become the dominant force in the market over the past decades. If I want to invest in financial services industry, it has to be a firm that will disproportionately benefit from this migration to alternative assets.

I’m currently working on a pitch about aircraft engine leasing, which is also an alternative asset. I’ve discovered that there are many opportunities in these industries, but they are extremely talent-driven due to the complexities requiring deep industry knowledge and unstructured finance that made them unqualified for vanilla public debt issuance; traditional banks just can’t get involved. If assets can be deployed into more alternative asset classes, the risk-return profile would definitely be better than what’s available on the market. For example, the engine leasing program currently generates yield around 8% before leverage, company level ROE reaches 20%+.

Now, considering the current environment—with 'higher for longer' interest rates and various uncertainties—I believe that being an equity investor now won’t yield excess returns, whether in public or private equity. True value investors in equities are rare; most equity investors tend to be gamblers or hedge funds. They made their money riding the broad U.S. beta, but after an economic adjustment, very few may survive if the Federal Reserve doesn’t step in. Conversely, credit investors are increasingly acting like true value investors—they focus on fundamentals and downside protection. I think they will win in this environment, and more funds will flow into fixed assets, which means that Apollo’s credit business will benefit. In fact, private credit isn’t as sketchy as many imagine; when I study restructuring, I find that senior secured loans typically aren’t impaired—they’re all repaying principal and interest. Hedge funds might step in to run through bankruptcy liquidations, but Apollo primarily invests in investment-grade credit, which should remain relatively unaffected. Moreover, if more opportunities arise in the market, they can react quickly and buy at the bottom.

"This is why I’m focused on this industry—because of both personal experience and my observations of the industry, along with macroeconomic thinking. I’m gradually validating my views through research. So, in this round of U.S. market adjustments, certainly some will be hurt, but the adjustment is good for these companies because they’ll expand market share and become stronger. I’m looking to find such companies, and if the price is right, we can gradually shift some of our positions from BYD into these firms."

Current credit cycle we are in:

While I don’t pretend to be an industry expert, it’s good to have basic knowledge on what stage of the credit cycle we are in. We are going to use NYU professor Mr. Altman (best known for Altman Z score in predicting corporate bankruptcies) chart on the current credit cycle we are in.

My conclusion is that the US leveraged finance market, and probably the European market, incurred an “Average” credit cycle performance in 2023, as several positives continued to manifest, offsetting the well published negatives of high inflation, elevated interest rates and a possible recession. These positives include still robust corporate revenue and cash flow growth, especially amongst firms able to pass along the escalating costs due to inflation to customers, a limited amount of bonds and loans that matured in 2023, and still high but declining inflation.

However, a lot has changed since the new administration. The tariff war is really hurting business fundamentals and investor/business owner confidence. As inflation remains elevated, economic growth is showing signs of slowing. The University of Michigan’s Consumer Sentiment Index fell 11% last month, dropping to its lowest level since 2022.

Consumers are growing increasingly concerned about their financial prospects. Sentiment is a key indicator of future spending behavior; when confidence declines, households often scale back discretionary purchases, which can slow overall economic activity. Consumer expects high inflation and Fed is reluctant to cut rates. The latest report showed a sharp rise in inflation expectations, with the one-year outlook climbing to 4.9%—the highest since November 2022—and the five-year outlook jumping to 3.9%, marking the largest monthly increase since 1993.

The worse case scenario is stagflation, and we are seeing more and more talks on the street as people wake up to the reality that US Exceptionalism may change. The productivity boost from AI might not come for years and tariff and inflation woes hurts right now. Overall, we are bearish on the credit cycle. We believe we will see more defaults coming to the high yields market and this will raise concerns on asset managers like Apollo who owns these assets (partially, majority is investment grade credit). This is the reason we chose to wait now ($160 level) as we see more corrections coming, but once the market bottoms it will be an attractive opportunity to build positions on Apollo at an attractive valuation.

Apollo’s investment philosophy centers around “Purchase Price Matters.” This is a great tradition learned during the founding years of private equity and enhanced since their transition to private credit. Talking to credit investors, they take their purchase price very seriously because that determines their downside protection, whether at the “create” price there is enough assets to cover outstanding liabilities. One of the main concerns we had on investors is an abundance of assets chancing down the yield and ignoring the inherent risk. When the cycle turns, those investors will be the first ones who face defaults. Apollo’s value focused investment philosophy convinces me that their asset quality is higher than industry average, their portfolio would be more resilient than investors thought. And we think Apollo will thrive during the down time putting more perpetual capitals to works at attractive yields. Apollo professionals have a reputation for distressed work-outs maximizing recovery and future interest for their holdings, creating above average returns in future that more than make up for the decline in downturn.

Inflation, unemployment, and decline in GDP

Generally observing an uptrend in high yield market default rate. And that’s predictable given the easy credit extended during government stimulus and companies are having trouble refinancing and servicing those loans at a higher rate. And this time there might not be stimulus coming.

Two most important metrics when assessing credit quality: Interest Coverage ratio and Leverage Ratio. Picture above showcased interest coverage ratio for high yield market declining, signaling weakness.

High yield default rate outlook by Standard & Poor made 2024 September. Now the broader market is leaning towards the bear case where more tariff, harder immigration policy triggering inflation and slower pace of rate cuts. Tariff will also impact company bottom line and they will have less growth.

Analysis on Apollo Management:

We are not going to pretend that we know more about the business than Apollo itself. They did an excellent job communicating with investors on their strategy and long term guidance. We recommend watching the investor day presentation to gain more insights to the business. We are only going to offer a high level analysis on the business.

Apollo main business line can be split between two divisions:

Athene (~$500bn AUM): the #1 Retirement Solution provider;

Apollo AM (~$200bn AUM): the #1 Alternative Asset Manager in Credit.

Apollo Global generates earnings from three sources: We prefer to keep things simple, so we primarily focus on SRE & FRE, treating the PII and other income like Wealth Management as a growth option.

~60% from Spread-Related Earnings (“SRE”): Athene receives money from its annuity clients and reinvests them into assets with ~1.5-2% higher yields while keeping the difference. Apollo AM manages this capital;

~35% from Fee-Related Earnings (“FRE”): Apollo AM is paid ~1.5-2% of the assets to manage third-party capital, mainly other institutional investors like pension funds, through its funds;

~5% from Principal Investing Income (“PII”): Apollo AM receives a 15-20% performance fee called “carried interest” for the overperformance of its funds.

Fee related earnings mostly benefitted from the broader inflow to alternative assets, specifically credit, and the outperformance of Apollo within credit that gave them the largest market share. Spread related earnings is more volatile, and that is dependent on how well Apollo can deploy these assets to generate above average returns, but we would like to point out that it has always been profitable. Annual earnings fluctuate based on the broader credit cycle.

The FRE Business: Broader trends powering AUM growth

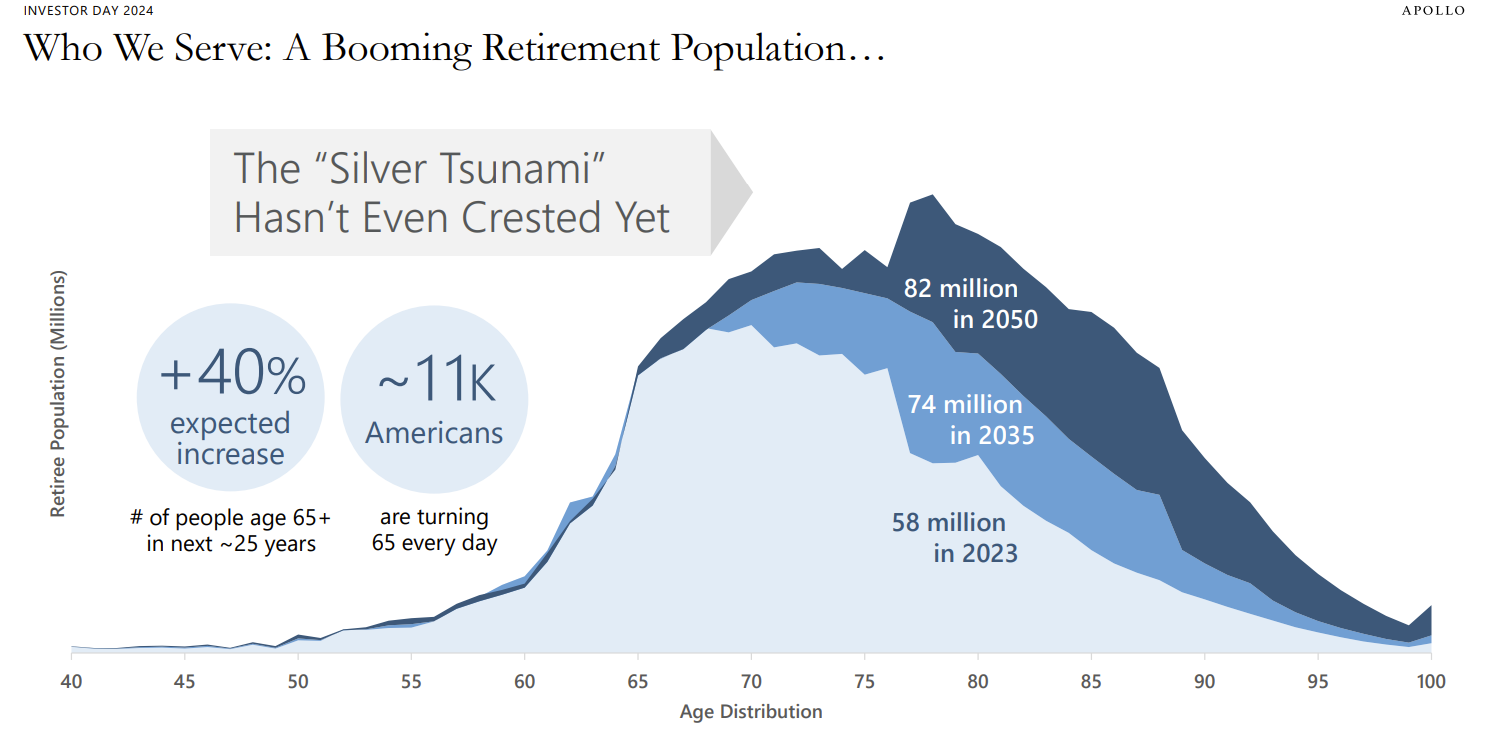

As society ages, huge demand for financial planning related to retirement. There is an acute need for higher yielding securities to compensate rising living cost.

The typical investment portfolio reimagined. Judging from current trends, we believe it’s the future because it delivered higher yields and better diversification. The world of investing is bigger than stock, bonds, and your house. There are so many options available and investors need to take advantage of this trend by increase their allocation to alternative assets.

Apollo has plenty of opportunities to deploy those capital:

Global industry Renaissance: Infrastructure, AI, energy transition, etc. requires huge fixed capital investments that requires long time horizon, most of it is investment grade. Private Credit IG is the future. It has to be a public and private solution.

Retirement: Why invest in daily liquid index when you don’t need the liquidity? Why pay the liquidity premium when you can get higher yield? We should include more alternative assets in the portfolio, not just equity and bonds and your house. Might need government approval to allow 401K to include private assets.

They need more diversification, Mag 7 is 35% of the index is just too concentrated, we don’t want American retirement to be levered to NVDA.

Individual: Family office allocates 50% assets in private assets. Moving to introduce private products to mass affluent and high net worth, offering more private asset products retaining the same advisors. More advisors need to get on the ship and educate investors.

Public v. Private: The burned stigma on private investments that they are risky. Both in investor base and asset managers.

No liquidity in public IG bonds since the financial crisis, takes five days to sell. Apollo starting a private trading desk to provide liquidity. There is also the first private credit ETF ticker PRIV that introduce private credit to public markets much like the bitcoin ETF. To conclude, it’s a huge TAM, lots of opportunities to deploy capital:

The SRE Business: Making Spread

One thing I would like to point out is the fluctuations in SRE. It does not always outperform! Investors got excited by the jump in SRE caused by the historical rate hikes. Apollo was able to capture that by transitioning from floating rate to fixed rate, locking in the high yields. What we are seeing now is the return to measured growth, so should the valuation be. But overall the higher for longer interest rate should benefit annuity sales which drives the FRE, and as long as Apollo can deploy those capital at excess returns, their SRE should grow more than FRE.

The spread is pretty consistent. Below average spread period is a great investment opportunity as it will reverse back, assuming the rigor of underwriting remains unchanged. Despite interest rate volatility, Apollo always adjusts within a short period.

As we can see, SRE spread is highly correlated with interest rate. If it’s on a steady uptrend, Apollo spread will be on an uptrend. Periods of stress will cause temporal dislocation between cost and yield on market, but it will always return to average. During uptrend Apollo raises capital at lower fixed rate and deploy them at higher rate locking in the spread, vice versa during sudden downtrend when fed push the rate to zero, Apollo takes a hit on their floating rate positions (hedge protected some) and find new opportunities to deploy capital at this new environment.

Invariably lower rate is bad for Apollo because allocation to annuities declines due to unattractive yield compared to equity, some might argue that lower interest rate lifts Apollo DCF valuations by reducing the discount rate, but I want to stick to the fundamentals.

• Yield on Deployed Capital:

When interest rates rise, the yields on loans, leases, or other credit products generally increase. For Apollo, if they deploy capital into credit instruments or leasing arrangements that adjust with market rates, the income generated from these assets will be higher.

• Cost of Capital Dynamics:

If Apollo has secured financing at fixed, lower rates or its cost of debt increases more slowly than market rates, a rise in interest rates will widen the spread between the asset yield and its funding cost. This differential directly boosts their spread-related earnings

Why stagflation might benefit Apollo:

The uncertainty in equity market would push more inflows to credit market looking for certainty in returns. And yields likely more attractive. (FRE inflow)

Stagflation tends to widen credit spreads because borrowers face higher financing costs amid slower growth, which can benefit Apollo’s credit investments by boosting the yield on deployed capital. (SRE spread)

This environment can offer attractive entry points for high-quality, investment-grade credits as well as distressed opportunities. (Hybrid instrument)

Apollo’s Core Advantage: Origination Machine

Apollo CEO Marc Rowan said: “The Constrain is not capital but the originations that matches the quality profile and meets their expertise.” And I agree with this statement. My father always told me there is no shortage of funding in China but good projects that delivers reasonable returns. This boils down the ability to deliver spread on origination and underwriting.

What is the moat of the business:

In origination that generates a premium compared to public IG credits. They have tighter control over the company financials and relationships that is important when negotiating pricing and terms.

in athene a long term retirement insurance provider that aligns the duration of the assets, not holding it on their own balance sheet.

In scale, need scale to be profitable, either big or very small hard to mid size player to survive. In capital, can write 10B dollar checks.

Also in track record of outperformance so you have something to show to investors, and reputable brand and talented management.

In investment philosophy that is highly recognized in Apollo. Investing in company is investing in management, especially in the asset management business. I resonates with Marc and Apollo’s investment philosophy that is very similar to that of Howard Marks and Warren Buffett.

Insurance is not asset gathering business, the assets you take under will crush you of its weight unless you can deploy it sufficiently to generate excess returns.

Important point mentioned is the cyclicality of capital deployment schedule, when there is opportunity we deploy more, when there is not like when interest rate is close to zero, we don’t lend or we only do floating rate products and take the losses for the upside gains in 2023. Careful underwriting discipline is what keeps company afloat, not just next cycle but the previous ones. And long term focus.

Two examples of seeing Apollo at work:

A stern alumni, recently came to STEBA, a club centers around entertainment and business, to tell us his career journey from investment banking at Goldman advising some of the largest entertainment corporations like Sony music and Universal to IPO to his transition to Apollo leading their music related business.

Milbank LLP advised Apollo’s (NYSE: APO) Capital Solutions business affiliate Redding Ridge Asset Management (“Redding Ridge”) on an asset-backed securitization (ABS) for global music company Concord. Redding Ridge and ATLAS SP Securities led on the investor syndicate for the new $850 million senior notes issuance, which is backed by a diverse catalog of music assets valued at over $5 billion

On Willis Lease Financing (Aircraft engine):

Air France-KLM and Apollo Global Management (NYSE: APO) today announced the signing of a definitive agreement for Apollo-managed funds and entities to make a EUR 500 million investment into an ad hoc operating affiliate of Air France that will own a pool of spare engines dedicated to the airline’s Engineering and Maintenance activities.

Risk quoting Net interest Apollo rising

Nevertheless, there are some fundamental differences between the two. Through its insurance business, Apollo has a resilient funding base, making it less reliant on capital markets to raise funds than GE Capital. The firm is run for spread, not for absolute earnings. And while there was speculation that neither Welch nor Immelt really understood the financial services business, that can’t be said for Rowan.

One feature the two firms do have in common though is complexity. GE Capital got mired in it; Apollo thrives on it. Apollo’s willingness to embrace complexity has been the source of a lot of value the firm has created over the years. “One way we create growth for a reasonable price is complexity,” proclaims Rowan. The Caesars Palace Coup recounts the story of how Rowan and his team navigated the intricacies of the casino operator’s highly complex restructuring.

“The search for returns was never ending,” write Gryta and Mann. “Capital was constantly on the hunt for deals to finance, assets to buy, and businesses to run. From taco stands to ocean freighters, they were putting GE’s money to work.”

But a number of problems served to undermine GE Capital. First, it grew too large. The unit could get higher returns only by shouldering more risk, causing it to go after acquisitions or new lines of business it earlier may have rejected. This became an issue because the business was run for earnings rather than for spread. General Electric itself prided itself on always making its numbers and GE Capital provided the mechanism to deliver that.

Marc Rowan of Apollo proposes another cause for the downfall: “If one looks back and thinks about some of the problems that GE and other concentrated originators of spread found, they relied too much on too few businesses.” Looking at GE Capital, it’s not clear that’s true. Rowan argues that 15 to 20 origination platforms is sufficient to diversify risk, but GE Capital had as many.

Valuation: Buying Low

Below is a pretty good valuation chart that I agree with:

https://alexandersteinberg.substack.com/p/magician-apollo-transforms-life-insurance

Using conservative valuation, assign 10x for SRE and 20x for FRE, assigning no value to principle and other growth business as they are not enough to move the needle. The valuation should be around $110 this year. This would put blended p/e ratio to be ~14x. This puts Apollo at a natural advantage because it’s valuation is the lowest among alternative asset managers due to a larger insurance presence, but it generates significant synergies which should be assigned a premium. Based on Apollo’s growth profile, assigning 1x PEG, should yield 17x+ long term .

And I do believe sector valuation will get lower because uncertainty surrounding the economy and portfolio investments. More default on high yield bonds is a clear indicator to follow. Fed might lower interest rate to prompt up economy which pressures the SRE business.

Quoting the author:

Certainly, I open myself to critique of using conservative multiples for FRE. For example, Ares (ARES) is trading at the FORWARD 40x multiples vs. my TRAILING 25x and ARES is arguably the best comp to figure out these multiples.

In this regard, I would like to remind you that multiples have not been always that aggressive. In early 2023 and 2024, the same ARES was trading at the forward multiples of 18 and 28 respectively. Secondly, my model worked pretty well in 2021-2023. In 2024, alt managers skyrocketed and are trading at multiples that are too aggressive for my taste.

Also, technical analysis shows the stock should find support at this level: $92-$110

The long term guidance issued by the company should double its business by 2029, so investors should expect mid to high teens IRR, coupled with buying at the cyclical low so some valuation appreciation, I believe long term IRR will cross the 20% hurdle rate.

In the direct space, the thing we love about it is that the documents are much tighter than the traditional BSL (broadly syndicated loans, a form of leveraged bank loans) market. And I suspect that since most of the market now is first lien, it's a bit deeper in terms of first lien, but the second lien market has really slowed down. I suspect a lot of the weakness and a lot of the losses will end up happening in the mezzanine and subordinated tranches. Which we have ... really, really pulled back.

When I took on the CIO role coming up on four years, we had about $6 billion of second liens. We have less than $1 billion now.We've really taken down our balance sheet. People don't realize our balance sheet today is close to 60% investment grade. On our retirement service balance sheet, it's 95% investment grade. So we've really gone senior and gone with less-levered companies. And really in our credit business, really gotten out of the mezzanine and subordinated tranche business.

In an environment of rampant inflation and rising interest rates, banks can indeed face significant headwinds. When the Federal Reserve raises rates, the market value of long-term bonds on banks' balance sheets typically declines due to their inverse relationship with yields. This mark-to-market depreciation can reduce the banks’ capital buffers, limiting their ability to extend credit. The situation is reminiscent of what happened with Silicon Valley Bank, where a concentrated bond portfolio and insufficient hedging strategies led to liquidity issues and constrained lending capacity.

For alternative lenders like Apollo, this scenario can present a compelling opportunity. If banks are forced to restrict credit due to balance sheet pressures, Apollo could step in to fill the credit gap. Given Apollo’s focus on alternative credit investments, its ability to deploy capital at higher yields, and its more diversified funding structure, the firm is well positioned to extend credit profitably during such periods. Essentially, while banks might struggle to maintain their lending levels under these conditions, Apollo could capture market share by providing credit solutions, benefiting from wider credit spreads and a relative flight to quality in the credit market.