Saia - Crown Jewel of Transport

https://www.horizonscapitals.com/s/Saia121.pdf

This is the powerpoint version of our research.

Industry Overview: LTL Dynamics & Market Consolidation

The less-than-truckload (LTL) industry has long been considered a low-growth sector in terms of volume and tonnage. The overall freight volume mostly increased in-line with GDP, boosted by E-commerce freight. However, the beauty of the industry is company grows through two levers: Rate increases and market consolidation.

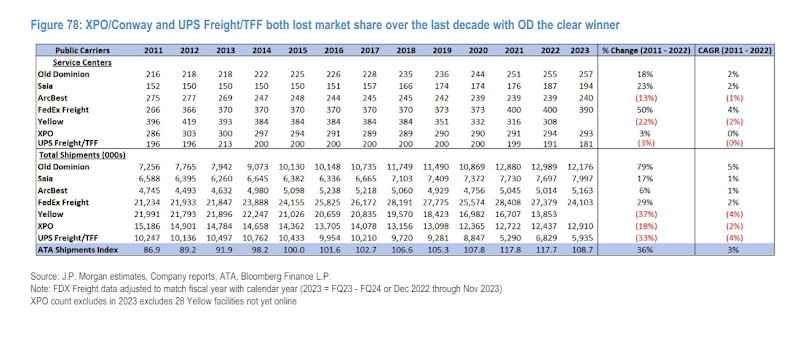

LTL market is a highly concentrated market with top 10 players accounting for 77%+ market share. It has a high barrier of entry requiring national infrastructure investments and fleet of local pickup and long haul drivers. Leaders in the industry, like ODFL and Saia, were family run with hundred years old history. They were less focused on short term profits and more focused on building a weather proof legacy - the kind of business with low debt leverage, national network of valuable logistics real estate, and in-house drivers and operators that treat their customers right. After the financial crisis, LTL players used pricing in an attempt to takeout their competitors that eventually blew a hole in everyone’s balance sheet. This taught the families an important lesson: never use pricing to resolve your problems, it may bring freight volume in the short term, but the margin compression that follows is just not worth it.

A new player, Old Dominion Freight Line (ODFL), has emerged from the crowd, championing service quality and on time rate with low claims ratio (fright damaged in transport). They were able to charge much higher pricing and customers are satisfactory with their service. It’s a successful business model that made the family billionaires and employees with stock options millionaires upon retirement. Most importantly, it shows its peers that focusing on service rather than just pricing is a much better alternative, there are enough butter for everyone to spread, given the freight volume is steadily increasing and cannot be replaced, and the fact that transportation only accounts for a fraction of the freight value and shippers are willing to pay premium for faster delivery and pickups. To this date, ODFL is still the leader in annual pricing adjustments and its Operating Ratio is the lowest (the lower the better, represents higher operating margin) at around 70s while the runner up like Saia is 80s, less profitable ones are in 90s, still more profitable than their Truckload peers.

The LTL industry now is like a cartel or a group that has tacit agreements on pricing and competition. Since there are only a couple national LTL service providers, they agree to not compete on price but on service. Another way to think about it is Game Theory, if all players chose to collaborate, they get the biggest reward, and that’s what LTL players chose to do. It’s rare to see this kind of tacit agreement, but in a developed economy, in a country on wheels, the LTL has effectively become a tax on all shippers, although the tax is insignificant.

The focus on service quality then asking customer for price increases is a repeated theme we see in industry research. It comes up again when we asked Roadrunner (See our Roadrunner article - zero to hero) Chief Strategy Officer what is his strategy to turnaround Roadrunner, he said “Service, service, service.” Equity analysts penalize those that took weaker pricing in exchange for freight volume, and rewards those that plays the service business model. The pricing premium allows LTL firms to invest in expensive real estate and logistics technology and additional linehaul capacity that reduces third party/locomotive handling of the freight, which results in faster deliveries and low claims ratio. This build up of infrastructure allows LTL firms to capture maximum upside when logistics cycles turned positive, and they were able to capture the increase in demand and issue multiple rate increases a year to increase their profit margins, as we can see the explosive growth opportunity during the post pandemic recovery (higher inventory + robust demand).

Recent structural shifts—particularly the market exit of Yellow and consolidation efforts by leading players—have provided a significant tailwind. Yellow is an union LTL provider that has the longest history and largest market share. They were mired by internal operating issues and conflict with union that resulted in a lack of investment in its infrastructure and deteriorating service quality. Eventually the problem got so bad that the company is worth more dead than alive as restructuring is infeasible with the conflict of unions.

The bankruptcy of Yellow and subsequent auction of its most prized real estate gave an immediate boost to second runner ups. The majority of the real estate were acquired by XPO, and Saia. Many of these real estate, although require significant capex to upgrade, are invaluable as local laws or regulations prevents construction of additional logistics real estate near city center and existing ones were either occupied or rented at a high rate. Yellow’s real estate gave a key piece of the puzzle to the runner ups to catch up to ODFL in terms of national scale and efficiency. It’s about two years or more of normal terminal expansion all happening in one year. And we believe these assets, although negative or below average profitability threshold for Saia, will shine in the next logistics cycle, resulting in higher yields and lower OR. It’s not a question of HOW, but WHEN the cycle will turn because history has shown that it always reverts. Saia’s earnings have been compressed in the short term by the acquisition of these assets and continued terminal expansion and capex commitments, but in the long term these will be high ROIC investments.

The LTL company XPO won 28 properties for $870 million. Estes Express Lines, who entered the auction with a lead bid of more than $1.5 billion for all Yellow properties, ended up winning 24 terminals for a combined $249 million. The Georgia-based trucking organization Saia acquired 17 Yellow properties following a $236 million bid.

LTL tonnage has shown strong correlation with U.S. industrial production (PMI), with key end markets including electrical equipment, machinery, and automotive components. While muted demand persists in the near term, reshoring and infrastructure spending could serve as longer-term catalysts for growth.

The current freight cycle, citing RXO’s coyote curve forecast for 2025 Q1:

Based on recent history and current market dynamics (shrinking but still available capacity, stable demand), it’s quite possible we’ll see a lower potential market peak; for guidance, a look back to 2014 would likely be a better comparison.

LTL pricing follows the TL market. Expanding when hot, and held off steady (slightly above inflation to cover reinvestment costs). I do have a more bearish outlook as tariff war continues. Could be like a 08 cycle in terms of premature peaking then immediately head off to rate decreases. The 21 mega cycle has drained the energy for the subsequent cycle that follows. Excess capacity need time to clear.

We believe the best time to invest in LTL, is when the cycle prematurely turns and investors were greatly disappointed by sudden bust of the freight recovery story. The stock price have been resilient during the down times due to price discipline and promise of future rewards. When that is not as expected, or perhaps delayed one or two years, people lost patient and leave, giving long term investors a great entry point. We like this business, and we are in this for the long haul. We are patient and the market has repeatedly rewarded those who are patient. Market price forecasts leads cyclical downturns one to two quarters ahead. Judging from current velocity and cyclical peak prediction, I think the TL/LTL sector has yet to reach its bottom or turning point, it would probably be in the third or fourth quarter this year.

Saia PE peaks around 30x and bottoms 16x, so currently is trading at 27x, another 35% decline would put the stock price around 240 and cyclical lows.

Another comp graph, as you can see the recent two cycles lifted valuations for all LTL companies above historical range due to the record intensity of the cycle and value capture during uptimes. If we forecast a return to normal scenario to previous cycle valuations like most recent 2019, valuation is around 16-17x. There is a gradual uplift of LTL cyclical low valuations given the improved industry dynamic and OR (expanded margins). There is also company level improvements like XPO’s new management and post spin-off refocus on LTL strategy. Saia is also a beneficiary as the company has improved its service and has more potential to charge for it subsequently, valuation will put that into consideration.

LTL pricing has steadily increased but tonnage has been weak that more than offsets the pricing and shipment gains. The spread between TL and LTL needs to tighten though, either through an improvement in TL pricing or muted price hikes, before LTL can further increase pricing, because some freights can be supplemented by TL if the spread gets wide enough that its more economical.

Amazon's LTL ambitions are no secret. The company has been posting job listings for LTL product managers and network design positions within its Amazon Freight division, signaling a clear intent to build out internal LTL capacity (Source: J.P. Morgan analyst Brian Ossenbeck, 2025). By leveraging its extensive network of cross-docks and existing logistics assets, Amazon can construct LTL operations, potentially reducing demand for rival carriers while simultaneously increasing demand in the truckload segment (Source: J.P. Morgan analyst Brian Ossenbeck, 2025).

This is a major risk to watch for, amazon does not succeed in everything, like groceries. But the story alone would compress valuations unless the sky are cleared.

SAIA’s Growth Strategy: Expansion & Pricing Discipline

Management has demonstrated a strong track record of executing growth strategies without margin erosion. Between 2017 and 2022, SAIA improved its operating ratio (OR) by 1,000 basis points and grew operating income by 38% annually, all while opening 41 new terminals and increasing total shipments by 15%.

Following Yellow’s bankruptcy, SAIA capitalized on an opportunity to acquire prime real estate, investing ~$244 million to purchase 28 terminals. Notably, high-value locations such as Trenton, NJ ($71 million) and Laredo, TX ($51 million) accounted for over half of the company’s acquisition spending. By year-end 2023, SAIA had 8,700 operating doors across 194 terminals, with the newly acquired properties adding ~976 doors, an 11% expansion.

For 2024, SAIA plans to bring 15-20 of these new terminals online, supported by record capital expenditures of $1 billion—equivalent to nearly one-third of annual revenue and double the capex intensity of 2023. Of this, $244 million will go toward terminal purchases, $300 million toward real estate investments (including site improvements and facility expansions), and the remainder toward fleet and equipment to support volume growth following Yellow’s exit.

Financial Forecast & Operating Leverage

Revenue Growth: We forecast 12.5% YoY revenue growth in 2024, assuming 18 new terminals become operational.

Operating Ratio (OR) Improvement: We project a ~225bps YoY OR improvement in 2025 as SAIA benefits from terminal expansion and a potential volume recovery in a rebounding freight market.

Long-Term Pricing Power: The LTL industry is highly consolidated, with the top 25 carriers controlling 90% of the market. This dynamic, particularly following Yellow’s exit, strengthens pricing power among leaders like SAIA, XPO, and ODFL. Industry players have demonstrated a commitment to pricing discipline, prioritizing service quality over rate competition.

Key Competitive Advantages

Economies of Scale & Network Density:

National scale provides higher profitability due to fewer competitors and more lucrative long-haul shipments.

High barriers to entry, as national networks require significant real estate investments and local regulatory knowledge.

Purchasing advantages in fuel, trucks, and insurance, benefiting larger players over regional operators.

Fixed cost leverage enables greater asset utilization and lower OR as volumes rise.

Premium Brand & Service Offering:

SAIA’s ability to charge a premium is rooted in its reliable service, on-time delivery, and minimal damage claims.

Expansion of service centers improves network efficiency, increasing freight visibility and reducing handling costs.

Higher density drives cost efficiencies (shorter routes, more direct shipments) and strengthens pricing power.

Operational Excellence & Execution:

SAIA is following a strategic path similar to ODFL, with disciplined execution and a long-term focus on price and service quality.

Investment in logistics technology and pricing algorithms ensures efficient capacity management and route optimization.

Further OR improvement into the 70s range would warrant valuation premiums comparable to ODFL.

Valuation & Investment Thesis

Attractive Entry Point: Current price levels (~$400) offer a compelling entry opportunity, with upside potential of 60% by 2026, implying a PEG ratio of ~1x.

Cyclicality & Earnings Power: Historically, LTL earnings power has been underestimated during freight downturns and overestimated during upcycles. As the trucking cycle recovers in H2 2024, we anticipate analysts will adjust expectations upward.

Margin Expansion Potential: SAIA’s OR improvements and pricing power suggest further earnings growth. We expect EBIT CAGR of ~25% through FY26, supported by strategic capex investments and disciplined cost management.