BYD - Build Your Dreams

BYD Investment Memo

Fundamental Analysis

To access our Chinese Original Blogpost on Snow ball Finance: https://xueqiu.com/3540620772/328098111

China's Annual Car Sales

Annual sales: ~23 million units. The market is stable, with the focus on NEV penetration rates and BYD’s market share.

Current NEV penetration: ~50%. Predicted to reach 80% within three years, supported by price parity, charging infrastructure, smart driving technology, and government policies.

There is really no reason to own a ICE in China, PHEV/BEV is in everyway superior, in terms of quality, ADAS, price range, economy, design, and brand, etc. Sure the BBA might be harder to push out, but their market share will dramatically contract as people don’t find their value proposition (selling their brand basically) attractive.

Unless you really like the smell of gas and engine, which PHEV can do as well! Plus an electric motor, compliments from the house!

Market Share Projections

Benchmark: Volkswagen (40-45% market share in Germany) and Toyota (30-35% in Japan).

BYD's estimated market share: 35-40% in China, supported by high entry barriers in hardware and smart driving technology.

Estimated sales: 23 million x 35% = 8 million vehicles.

Alternative calculation: 18.5 million NEVs (80% penetration) x 40% market share = 7.5 million vehicles.

Low-End Market Perception

High-end vehicles (above 300,000 RMB) account for less than 15% of the market.

BYD’s focus on affordability aligns well with broader market demand.

III. Overseas Sales Projections

Benchmarking Toyota

Toyota’s overseas sales: 7-8 million units. BYD aims to achieve similar scale as it expands globally.

Current overseas capacity: ~1 million units, expected to increase with the 40 billion RMB financing plan.

Global Market Analysis

JP Morgan 2030 Chinese auto global export forecast: 7.5-9.5 million units.

Potential U.S. market expansion via local manufacturing partnerships.

Current overseas sales: ~12% of total. Target for 2024: 800,000-1,000,000 units.

Projected Overseas Market Share

Estimated overseas sales: 8 million (domestic) x 30% = 2.4 million units.

Potential increase to 3 million if overseas factory plans are fully implemented.

Global market share: 40% of overseas NEV sales, which aligns with domestic dominance.

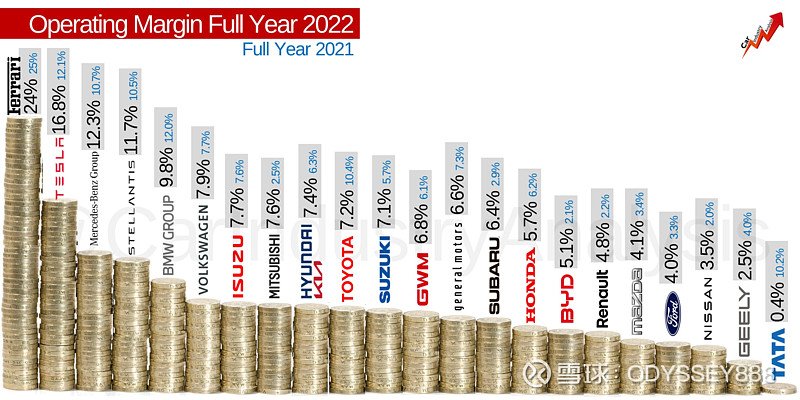

IV. Profit Forecast

moving up the margin chain 5% to 9% world class level.

Profitability Growth

Estimated 2024 profit: 43 billion RMB (adjusted to 38.5 billion after removing BYD Electronics' contribution).

Per-vehicle profit: ~9,000 RMB. Potential 50% improvement to ~13,500 RMB per vehicle.

Estimated 2028 profit: 140 billion RMB.

Alternative Profit Calculation

Domestic sales (8 million) x 12,000 profit per vehicle = 150 billion RMB profit.

Conservative estimate aligns with projected profit targets.

Accounting Considerations

Accelerated depreciation schedules reduce short-term profits but hide underlying profitability.

As depreciation phases out, profit growth will accelerate rapidly.

As you can see without depreciation and amortization charges BYD gross margin steadily increases, unlike the current GAAP margin, reflecting the impact of accelerated depreciation and elevated short term capex.

The Capex investment reached unfathomable 100B RMB last two years to build capacity to fulfill market demand. BYD’s production capacity rose from sub one million to over eight million by the end of this year. Future investments would be much smaller, although still above industry average.

V. Valuation

Fair Valuation Multiple

Manufacturing leaders generally warrant a PE ratio of 20-25x.

Using a profit estimate of 150 billion RMB and a 23x multiple, BYD’s valuation is projected to be 3.5 trillion RMB.

Technical Analysis

Wave theory suggests the stock is in its second wave, with a target price range of 600-650 RMB.

Continued expansion into AI, autonomous driving, and new markets could push valuation even higher.

The third wave should push the stock to the thousands, after short period of adjustments.

VI. Conclusion

BYD’s comprehensive industry chain integration, strong market share in NEVs, aggressive overseas expansion, and conservative accounting practices present a compelling investment case. A threefold increase from the current 400 RMB share price to over 1000 RMB is realistic, backed by robust fundamentals and growth potential. BYD is well-positioned to become China’s most valuable and globally recognized manufacturing brand.

BYD Auto (BYDDY 1211.HK) - Investment Thesis by David Zhou - 1/24/2024

Why Invest in China Equities, Why in EV?

The Chinese equities market has significantly underperformed the global equities index, with the Hang Seng index reaching a historic low of 15.6 PE. Foreign investors are trimming their stakes in China, as cumulative inflow to the mainland Chinese market has declined from a peak of 233B Yuan in 2022 to 13B Yuan.

Given the pessimistic economic outlook caused by property deleveraging and frequent government crackdowns, I believe part of this capital outflow is warranted. Property deleveraging reduces household wealth and weakens consumer confidence, leading to slower economic growth, while government crackdowns create regulatory uncertainty that discourages foreign investment. These factors collectively contribute to capital outflows as investors seek more stable and predictable markets. However, there are high-quality companies located in fast-growing sectors like EV that are wrongly downgraded, making now an attractive time to buy and wait for market sentiments to improve and businesses to deliver above-consensus growth.

My Rationale for Choosing the EV Market

Global EV Revolution & China's Manufacturing Strength: The global EV revolution has just begun, and China has the best EV manufacturing ecosystem that produces a huge volume of cars at the lowest price. Similar to investing in AI companies on NASDAQ, if investors want to capitalize on the EV opportunity, they have to invest in Chinese equities.

Favorable Policy Outlook: The Chinese government supports auto manufacturing as it creates jobs and has enough scale to become the second growth driver counterbalancing the deleveraging impact from property.

Industry Consolidation & Market Share Gains: The competition landscape has cleared with winners like BYD continuing to consolidate market share (BYD Auto controls 36.6% EV market share, up from 17.1% in 2021). BYD is at a critical inflection point driven by scale, brand diversification/premiumization, international expansion, and self-driving software.

BYD’s Competitive Advantage

1. Vertical Integration: 75% of Parts Are Sourced Internally

BYD is the most vertically integrated EV manufacturer, and its competitors have no chance of reaching the same level and scale. This gives BYD a significant cost advantage (Wright’s law: production doubles, cost reduces by 15%), providing the strongest moat in price-sensitive markets (below $30,000).

For reference, BYD is the second-largest battery producer with a 15.7% market share. It has its own semiconductor fabrication plant, the largest in China. BYD Electronics ranks second to Foxconn. It is also the largest commercial EV manufacturer, supplying electric bus fleets and forklifts.

It generates over 10,000 Yuan ($1,500+) of net profit per vehicle, while competitors like Xpeng lose 112,500 Yuan ($16,071) per vehicle due to higher production costs, lower manufacturing efficiency, and aggressive pricing strategies aimed at capturing market share. Despite market concerns on price competition, BYD’s gross margin expanded to 20.67%, exceeding Tesla’s 17.89%.

The next stage of growth will be unlocked once supply chain capacity has fulfilled internal demand and begins supplying parts to external parties. BYD is actively partnering with other EV makers like Tesla to supply battery packs for Model Y. The higher gross margin and additional scale benefits will be accretive to overall earnings.

2. Launch of Premium Brands & Product Cycle Enhancement

Last year, BYD launched two premium brands: YangWang, with a medium price point at 1.1M Yuan ($160k), and Leopard, with a medium selling price at $60k.

The successful launch of a luxury brand is highly margin accretive and uplifts the entire brand image. The brand portfolio/diversification strategy allows BYD to capture customers across different price ranges. It is now selling cars as low as $10k to as high as $160k.

This year marks a new product cycle. BYD is expected to launch over 10 new cars featuring key technology upgrades like Blade Battery 2.0 and a new AutoDriving upgrade. This much-anticipated product cycle enhancement will increase the ASP of its vehicles and boost competitiveness, driving higher sales. BYD has not launched a new platform upgrade in two years.

3. International Market Expansion: Blue Ocean Strategy

Expanding into Untapped International Markets: BYD is venturing into Thailand, Brazil, and the EU market. EV penetration outside China remains in the single digits primarily due to a lack of affordable EVs. BYD’s entrance will alter the local EV market landscape by introducing competitive models that are both affordable and of higher quality compared to ICE-converted models.

Growing Global Market Presence: BYD is already the largest EV brand in Thailand and Israel, and its products are highly regarded in the Australian and EU markets.

Infrastructure & Supply Chain Investments: BYD is building its shipping fleet and constructing factories overseas to support its ambition to dominate the global EV market. The manufacturing, transportation, and dealership distribution pipeline is positioned for accelerating growth. Currently, some markets have only one BYD model available, but this is expected to increase to three to five models as supply chain issues are resolved.

Export Profitability: According to analyst estimates, exporting vehicles has 3X the profitability compared to domestic sales. Exports are expected to account for 15-20% of total sales volume this year, with an outsized impact on per-unit profitability.

Valuation and Target Price: Large Discrepancy Creates an Attractive Opportunity

The average target price from 29 analysts is 296 HKD, while BYD is currently trading at 180 HKD, representing a 65% upside. Analysts derive these estimates using discounted cash flow (DCF) analysis, comparable company valuation, and earnings multiples, factoring in growth expectations, profitability, and market trends.

BYD is trading at 13.75 PE for FY24, lower than traditional ICE manufacturers, despite being in a high-growth sector.

Given the strong growth pipeline and the impending autonomous driving revolution, the market has significantly mispriced BYD.